Despite the geopolitical shock involving Iran, investors’ optimism continues to rest on a central narrative: the transformative potential of artificial intelligence (AI) as a new engine of global growth. However, the rise in long-term yields paints a more cautious picture. This divergence between equity market optimism and bond market prudence is a defining feature of the current macro-financial environment.

AI as a key pillar

The conflict in the Middle East has deteriorated the macroeconomic equilibrium. Global growth forecasts have been revised downward, while inflation is likely to remain well above pre-pandemic norms for some time.

Yet, this shock has not fundamentally altered the perception of a resilient global economy. The global manufacturing PMI1 posted 52.4 in May, above its neutral 50 mark for the tenth successive month2. The production sub-index ticked up to 53.52, signalling the fastest rate of expansion since July 2021, although businesses continue to cite a temporary lift from precautionary demand. What’s more, the sanguine outlook is supported by the growing influence of the AI boom which is increasingly viewed as a structural driver of both growth and corporate profitability.

This investment cycle is often compared to past technological revolutions, with the potential to generate substantial productivity gains over time. Trillions of dollars are expected to be invested in AI-related infrastructure in the coming years, particularly in data centers, computing capacity, and energy systems. As a result, AI is no longer merely a technological trend but a core macroeconomic force shaping expectations for growth, earnings, and financial market performance.

However, this optimism raises important questions. The timing and distribution of AI-related gains remain uncertain, while the scale and capital intensity of the investment cycle introduce significant risks.

Bond markets signal caution

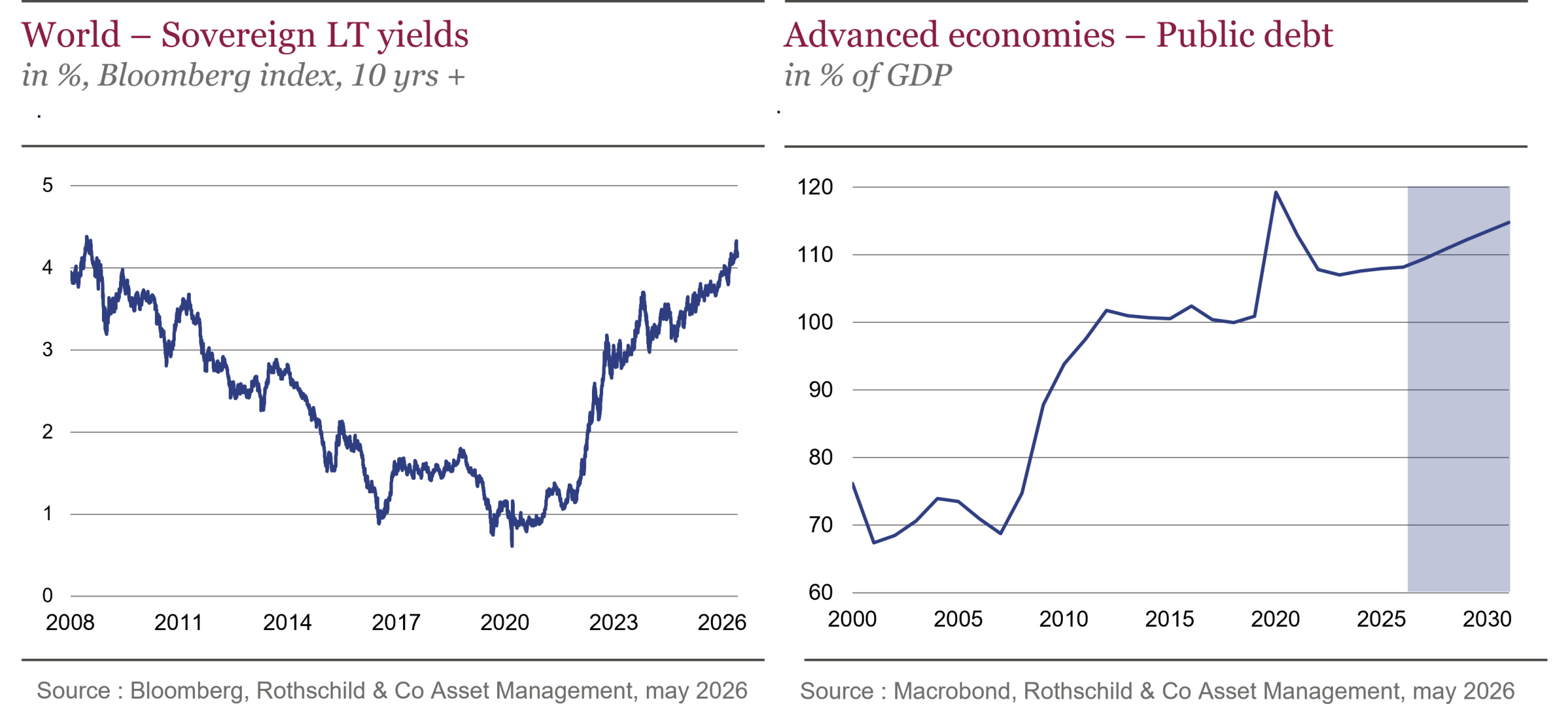

Sovereign bond markets are sending a far more cautious signal. Long-term yields have risen significantly, in some cases despite stable or easing policy rates. This reflects three overlapping concerns.

First, fiscal sustainability is becoming a central issue. Public debt levels are historically high, and governments continue to run sizeable deficits, driven by structural spending, geopolitical pressures, but also higher interest burdens. Indeed, as borrowing costs rise, fiscal consolidation becomes more challenging, reinforcing investor concerns. Rising yields therefore reflect both a higher term premium and the increasing supply of government bonds.

Second, the AI investment cycle itself is contributing to upward pressure on yields through its substantial financing needs. The scale of capital required implies sustained competition for savings. AI-driven IPOs—such as the anticipated listings of OpenAI or Anthropic, potentially raising tens of billions of dollars—illustrate these unprecedented funding requirements. While echoing earlier technological waves such as the dot-com or cloud cycles, the magnitude is significantly larger, leading to increased debt issuance and a potential rise in equilibrium real interest rates.

Third, inflation dynamics remain a key concern. The disinflation process that began in 2023 had clearly stalled in many economies even prior to the Iran-related shock. Looking ahead, several factors are likely to sustain upward pressure on prices.

Energy remains the most immediate driver. The Middle East conflict has triggered supply disruptions and heightened volatility, pushing prices above pre-conflict levels. Given energy’s central role in production and transport, this has broad second-round effects across the economy.

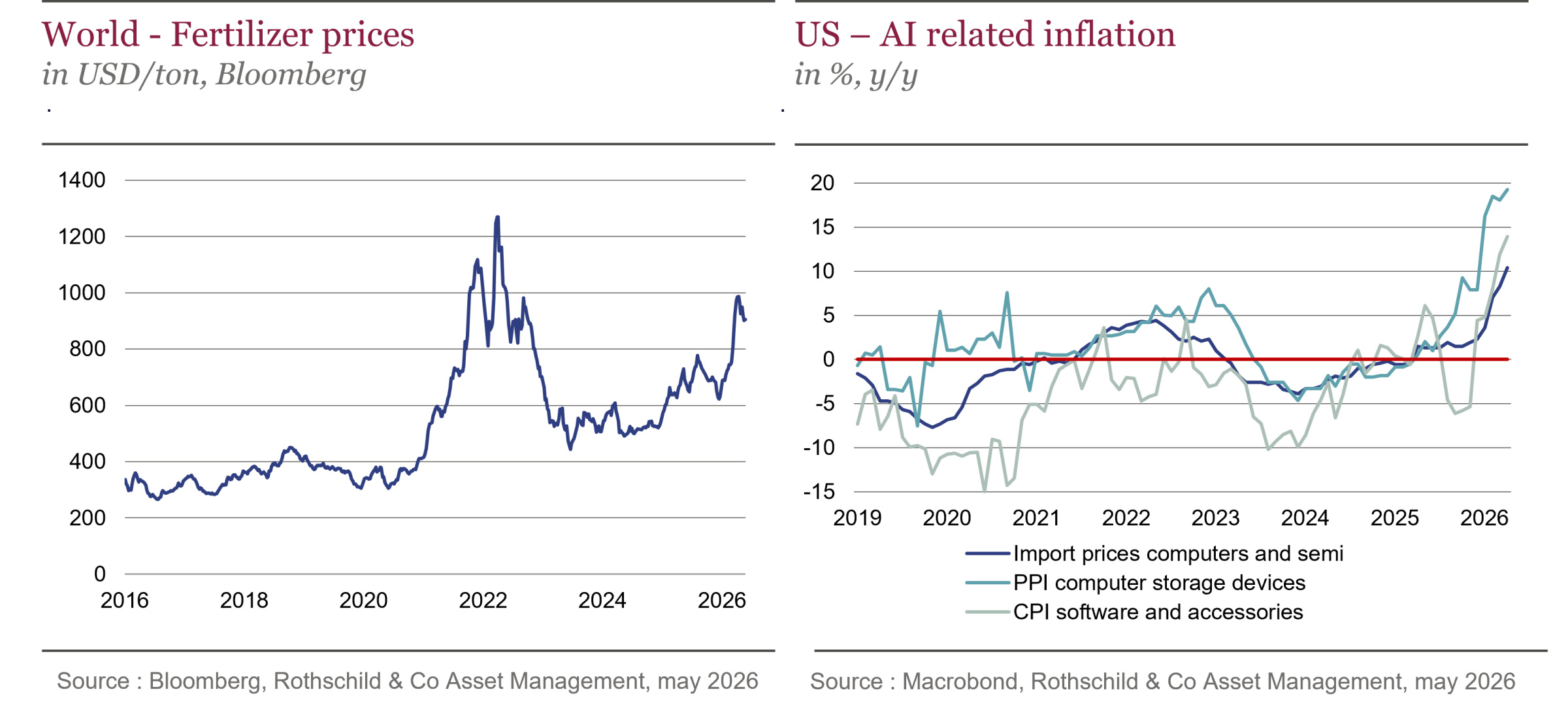

Food inflation is also a growing risk. Disruptions to fertilizer supplies, partly linked to geopolitical tensions, are raising agricultural costs and could weigh on yields. In addition, weather-related shocks—such as drought conditions in major producing regions like the US—represent a significant upside risk to food prices.

Despite some post-pandemic improvements, supply chains remain fragile. The current conflict has reintroduced bottlenecks in logistics and transportation, while industrial policies and geopolitical fragmentation continue to reshape global production networks.

Finally, AI deployment itself exerts short- to medium-term inflationary pressures. Its development requires massive capital expenditure, generating strong demand for inputs, infrastructure, and energy.

In this context, inflation should not be seen as purely cyclical, but rather as the outcome of interacting structural forces.

Risk of prolonged monetary restrictiveness

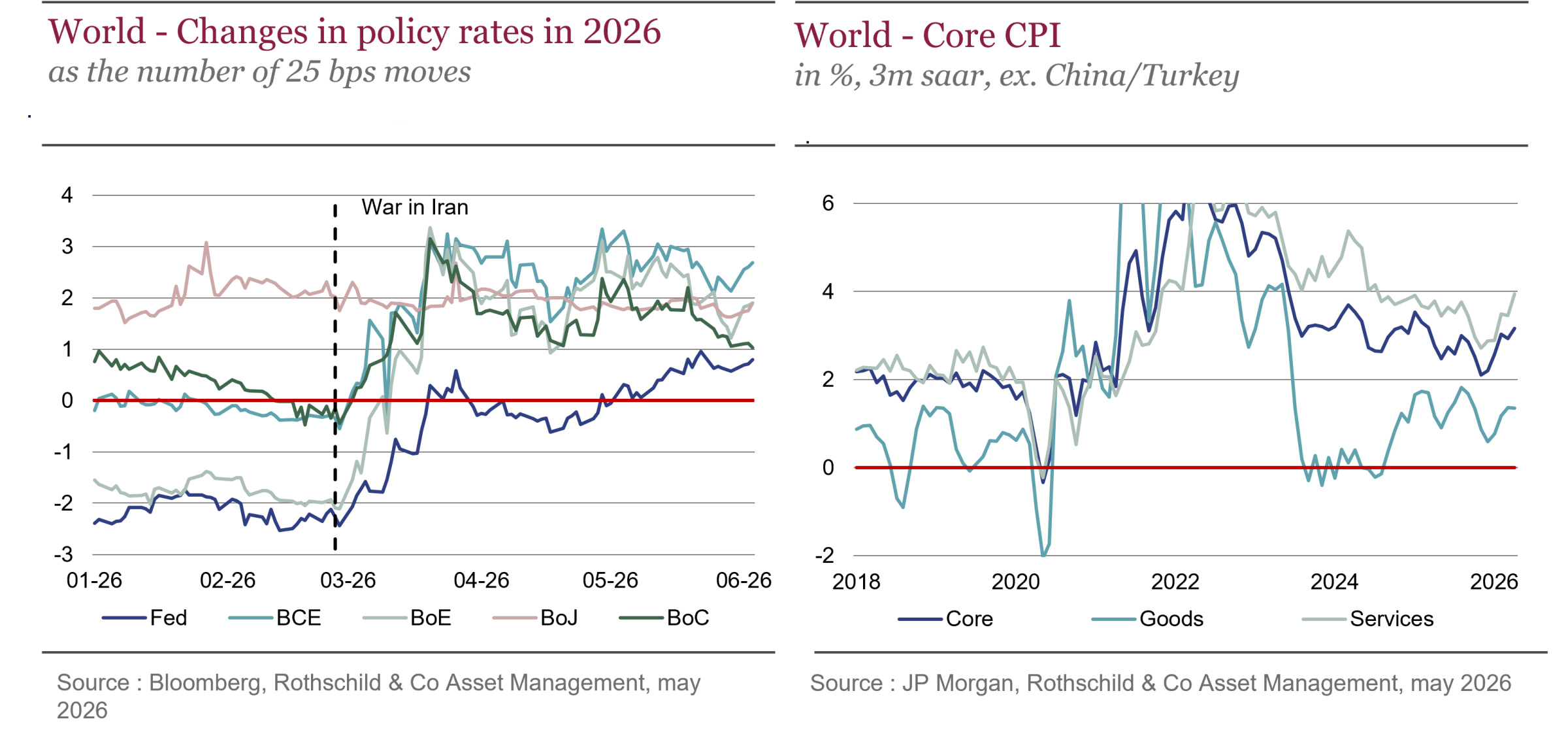

Against this backdrop, the outlook for monetary policy remains highly uncertain. Markets are currently pricing in only limited tightening in major economies, assuming that inflation pressures will prove temporary.

However, persistent inflation and recurring shocks suggest that central banks may need to remain cautious. Over recent years, the global economy has been hit by successive waves of supply shocks. In theory, central banks should look through them; yet with inflation above target for more than five years, it is legitimate to question whether the cumulative impact of these shocks risks de‑anchoring inflation expectations among economic agents.

The policy trade-off is therefore acute: further tightening risks exacerbating the growth slowdown, while premature easing could entrench inflation. Central banks must remain both vigilant and flexible. The risk is that policy rates stay higher for longer than currently priced in, thereby prolonging restrictive financial conditions.

For more information, visit Rothschild & Co AM website.

[1] Purchasing Managers’ Index (PMI), an indicator reflecting the confidence of purchasing managers in a particular industry. A reading above 50 indicates expansion, while a reading below 50 indicates contraction.

[2] Source: Bloomberg, May 2026.