Private credit and broadly syndicated loans are often mistaken as being similar, despite key differences in investment characteristics, market structure, valuation, and liquidity. Portfolio Manager Denis Struc and EMEA Client Portfolio Manager Lead Kareena Moledina explain why these distinctions matter for CLO investors.

Private credit and broadly syndicated loans are not interchangeable

Recent developments in private credit have brought two issues into sharper focus: liquidity and valuation. Redemption pressure has risen in semi-liquid private credit vehicles such as Business Development Companies (BDCs), while several abrupt individual private credit write-downs have highlighted how slow-moving valuations can obscure underlying credit deterioration.

This is why it is important to distinguish private credit from broadly syndicated loans (or BSL) rather than treating the two as interchangeable forms of leveraged finance. Both markets finance below-investment-grade companies, and both often fund sponsor-owned businesses, but they differ materially in borrower profile, market structure, valuation framework, funding and liquidity mechanisms (Figure 1).

That distinction is particularly important in the context of Collateralised Loan Obligations (CLOs). CLOs are built on broadly syndicated loans and funded through term liabilities, where a CLO issues tranches of debt and equity with defined maturities. This means the investor experience is fundamentally different from that of some private credit vehicles that offer periodic liquidity against inherently less liquid underlying assets.

Nevertheless, it is worth noting that private credit is not a homogeneous asset class. Asset-backed financing, for instance, is supported by a pool of assets, generally with more predictable cash flows and security. This segment is not part of current market concerns around private credit and is therefore outside the scope of this article.

Private credit versus broadly syndicated loans

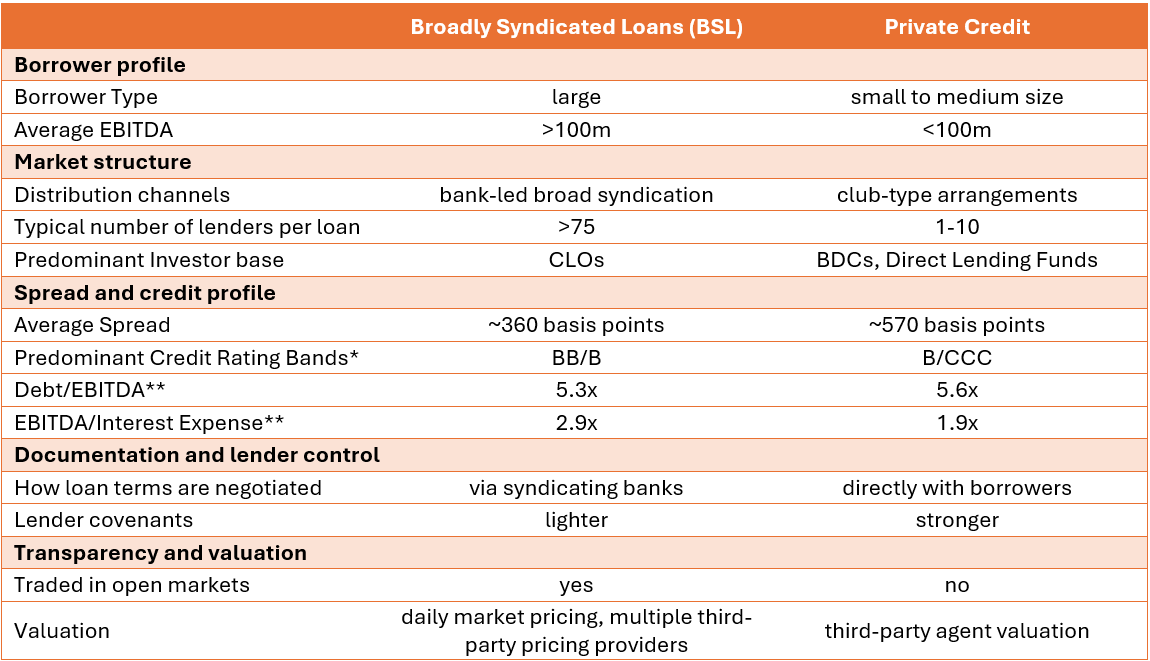

Figure 1: ‘At a glance’ summary of broadly syndicated loans compared to private credit

Source: Janus Henderson Investors, Morgan Stanley, as at 18 March 2026. Past performance does not predict future returns.

* Rating bands are intended as an indication of relative quality, noting that private credit is typically unrated or privately rated.

** Private credit reflects the Fitch average across sectors reported by Morgan Stanley Research; BSL reflects generic single‑B rated credit reported by Morgan Stanley Research, as at Q4 2025.