Schroders’ Global Unconstrained Fixed team constateert dat de productiesector in 2024 duidelijk stabieler van start is gegaan. In de afgelopen maanden heeft het team al aangegeven dat de sector zijn dieptepunt zou bereiken om daarna te verbeteren, wat nu duidelijker zichtbaar is in de leidende indicatoren.

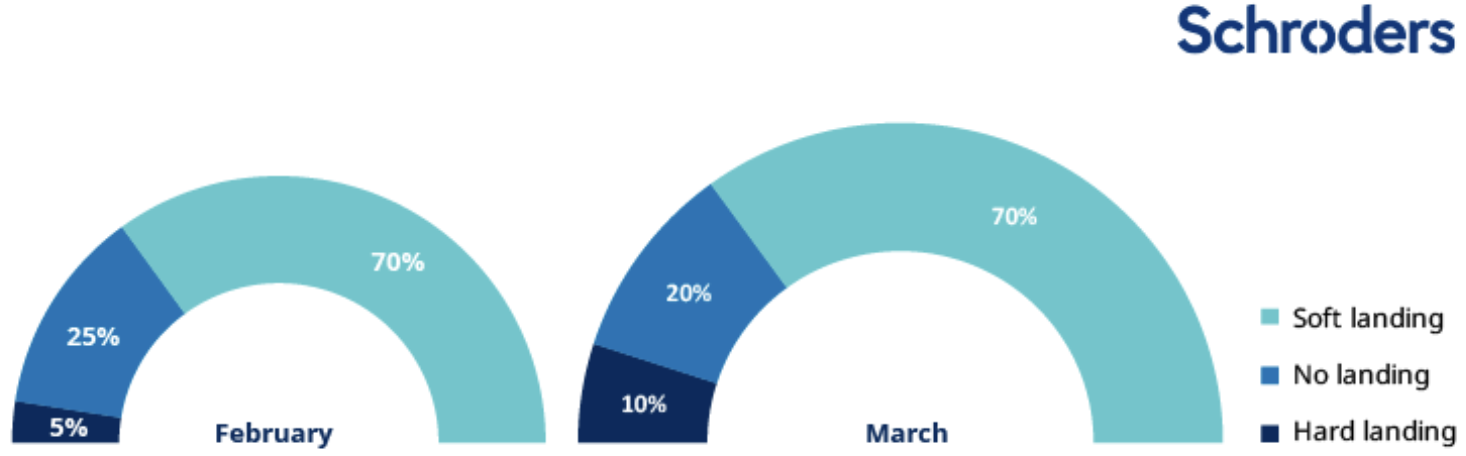

Deze opwaartse trend is in lijn met een 'zachte landing'-scenario, en het is onwaarschijnlijk dat dit zal leiden tot de oververhittingsproblemen die de productiesector in 2021 en 2022 ondervond. Ook de Amerikaanse arbeidsmarkt lijkt minder vatbaar voor oververhitting. Als gevolg hiervan heeft Schroders de waarschijnlijkheid van het ‘geen landing’-scenario verlaagd en het risico op een 'harde landing' enigszins verhoogd.

Lees hieronder de visie van het Global Unconstrained Fixed Income team op het macro-economische klimaat en hoe evoluerende scenario's opnieuw worden beoordeeld.

Is the "no landing" scenario being abandoned?

Not quite, but we believe its probability might have reached its peak. The labour market plays a critical role in both policy-making and our scenario probabilities. Signs of moderation have led us to decrease the risk associated with a 'no landing' scenario, while slightly increasing the risk of a hard landing. In essence, the tighter the labour market, the higher the risk of "no landing". Recent developments suggest a reduced risk of the US labour market tightening again, with more evidence pointing towards it easing.

The US quits figure, which measures the number of voluntary job leavers as a proportion of total employment, is one of our favourite labour market indicators. This figure continues to moderate and is now lower than the levels seen in 2019. Furthermore, small business hiring intentions, as measured by the National Federation of Independent Business survey, have significantly slowed since the end of the previous year.

Things are improving steadily

Improvements in the leading indicators of the global manufacturing cycle are being driven by a potent cocktail of easing financial conditions, stimulative fiscal policy and a supportive boost from defence spending amid escalating geopolitical tensions. These factors are unlikely to reverse quickly. We believe they are indicating a moderate rebound in line with a soft landing.

In the Eurozone, too, leading indicators are pointing to clear improvement, as the peak impact of monetary tightening recedes in the rear-view mirror. Given how weak growth expectations are for the region, it's relatively easy to exceed them with positive surprises. However, the persistent nature of inflation, with the disinflation progress made in 2023 stalling this year, serves as a cautionary note.

The deteriorating inflation dynamics are unlikely to hinder the commencement of the European easing cycle. The European Central Bank (ECB) seems committed to a rate cut in June, regardless of circumstances. However, they do imply potential challenges in the long term. We believe the market is anticipating too many rate cuts, too soon, following June.

What does this mean for portfolio positioning?

Our view on overall duration (interest rate risk) has been upgraded as valuations have improved over the past month, particularly in the US. The sell-off of bonds, coupled with the reduced probability of a "no landing" scenario, makes the outright yield levels appear more appealing.

Given the improving economic outlook in the eurozone, the potential for persistent inflation, and relatively high valuations, we prefer to be short on German bunds on a cross-market basis, especially against UK gilts. We maintain our core positioning for a curve steepening dynamic, although we slightly adjust our score on the US curve. While it still provides upside from current levels, it's less than what we previously targeted.

In terms of asset allocation, our strongest conviction continues to be in covered bonds. As for corporate credit, our negative scores remain unchanged for both US investment grade and high yield, reflecting persistently unattractive valuations. In the eurozone, the strong performance of investment grade credit has weakened the argument for favourable valuations, but we still hold a positive view.

De Unconstrained fixed income views: March 2024 is hier na te lezen.